By Jumana Saleheen, Ph.D., Vanguard European chief economist

- The global economy could face a tipping point this winter, as demand for fuel rises and the geopolitical battle over Ukraine intensifies.

- Restrictions on the flow of Russian gas to Europe are likely to be bad news for energy prices and threaten to push the already weakening EU economy into recession.

- With more challenging times potentially ahead, it’s more reason for long-term investors to have a strategic mindset.

It doesn’t appear that the war in Ukraine will stop anytime soon. As sanctions continue to hurt Russia’s economy, there is an ongoing fear that Russia will restrict the energy that it supplies to Europe.

We believe the energy crisis is likely to get worse before it gets better – so much so, that we see a tipping point for the global economy this winter, when demand for heating fuel is likely to rise as it gets colder across the developed northern hemisphere.

The map below illustrates just how big a supply shock Russia could potentially unleash as the world’s second-largest producer of oil and gas, accounting for 11% of the world economy’s oil and 15% of its gas.

The chart also shows how the US economy – an economy that is self-sufficient in oil and gas – is relatively insulated from the potential fallout compared with other parts of the world. It is a theme we explore further over the remainder of this article.

Eliminating Russian oil and gas would create a huge supply shock

Source: Vanguard, IEA as of 18 July 2022. Note: Refers to 2021 oil and natural gas production.

The energy threat is most acute on the European mainland, especially in central and eastern Europe, which has a high dependence on Russian gas supplies. Revenue from gas exports accounts for about 2% of Russia’s GDP, compared with 10% for oil exports. The smaller revenue from gas means Russia may decide to further use its gas supply to increase pressure on Europe against the sanctions imposed since the start of the war in Ukraine.

Recession triggers

As of 27 July, the Nord Stream 1 pipeline – through which more than a third of the Russian gas to Europe is supplied – was reportedly running at just 20% of its total capacity. Such low levels of gas flow will become a worry if they persist for an extended period. Our analysis suggests that if gas flows were to remain below an average of 30% of total capacity for a period of six months, it would tip an already-weakening European Union (EU) into recession – with Germany and Italy among the worst-hit member countries.

The way that the impact of lower gas supplies will be transmitted across the European economy is two-fold. On the demand-side, reduced access to gas supplies will lead to even higher energy prices and higher fuel bills. This will push up already-high inflation and take a bigger bite out of business profit margins and people’s real disposable incomes. On the supply-side, it will lead to constraints as gas quotas are likely to be imposed on different industries, as well as, potentially, households. Unable to maintain production at existing levels, businesses dependent on gas supplies might have to reduce hours or lay off workers.

EU member states have already agreed to commit to a 15% reduction in their gas demand this winter, albeit with some exemptions and lower targets for some countries less dependent on Russian supplies. But these are voluntary reductions that may become mandatory or may be increased in the months ahead.

The table below summarises how we expect the euro area economy to perform depending on how gas and oil prices behave over the next few quarters. Our base case, still, is for Nord Stream 1 gas flows to average between 30% and 60% of capacity over the second half of 20221. A persistent fall in gas flows below 30% would put us in the downside scenario with gas prices spiking, pushing up on inflation and pushing the economy into recession.

Economic outlook for euro area based on different scenarios for Russian gas exports

Source: Vanguard, Bloomberg as of 29 July 2022. *Based on Dutch TTF natural gas prices, which averaged 98 EUR/Mwh from 1 January 2022 to 30 June 2022. **Based on Brent oil prices, which averaged 105 USD/barrel over the same period.

Spillover effects to the global economy

An intensification of the European energy crisis will have negative implications beyond Europe too as it will push up global fuel prices and add to inflation, which is already at multi-decade highs.

As such, a ‘Russian winter’ could make it harder for central banks to tame inflation. It would be yet another unlucky supply-side shock to the global economy. It would risk entrenching economies around the world with the current combination of weak growth and high inflation – potentially pushing them into stagflation.

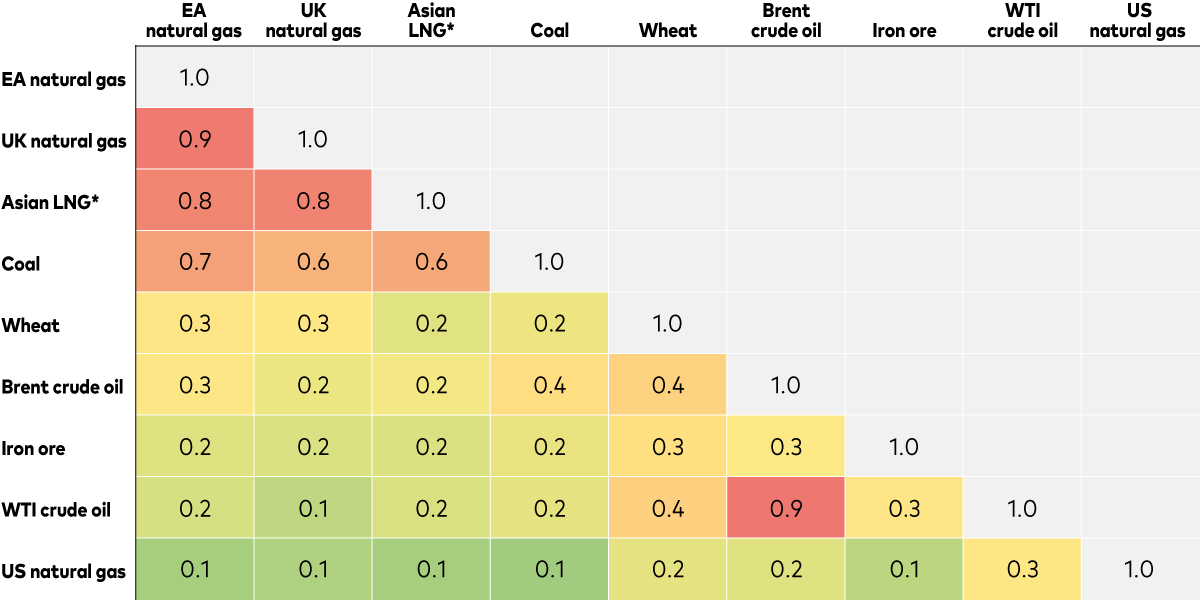

Our analysis shows that the UK and Asia are most vulnerable to any rise in EU natural gas prices. To illustrate that, the table below shows the statistical relationship over the last six months between natural gas prices in the euro area and other key commodity markets – it shows their ‘correlation’, which measures how much the performance of one market mirrors another. The closer to one the numbers are, the greater the sensitivity. The table suggests that a 10% rise in EU natural gas prices could be associated with a 9% rise in UK gas prices and an 8% rise in Asian LNG* prices.

The spillover from EU natural gas prices is highest in Europe and Asia

Source: Bloomberg and Vanguard as of 28 July 2022. Notes: Correlations are measured by daily change from 1 January 2022 to 28 July 2022. Red indicates a higher correlation and green a lower correlation. *LNG – liquified natural gas.

The impact on US natural gas prices, on the other hand, is more limited as the correlation is close to zero. This low correlation is partly because the US is itself a net exporter of natural gas. It’s also because of the segmented nature of gas markets. Gas is harder to transport and store – it must be transported via pipelines and stored in special facilities; or it must be liquified before transportation.

Oil, by contrast, is a more tradable good than gas – it can be put in a barrel and shipped anywhere.

Still, there can be some smaller knock-on effects from gas prices to oil prices and to other forms of energy, such as coal. This arises because firms and households who are able to substitute away from more expensive fuels to cheaper ones will do so. That increased demand will, in turn, push up crude, diesel and petrol prices from already elevated levels and add to the pressure on the US economy.

Restrictions on the flow of Russian gas to Europe are likely to be bad news for energy prices and threaten to tip the EU economy into recession. The effects will be felt in global energy markets, particularly in Europe, including the UK, and also in Asia. While US gas prices are largely insulated, US oil prices may not be.

There may be even more challenging times ahead. It’s more reason for long-term investors to have a strategic mindset – to remain focused on their goals and on what they can control, such as costs, and to stay disciplined and diversified.

Lulu Al Ghussein contributed to this article.

1 This base case is consistent with the recession probabilities published in our mid-year economic and market outlook, for a 50% chance of recession for the euro area economy over the next 12 months and 60% over the next 24 months.