Key points

- The US Federal Reserve has cut its policy interest rate for the first time in four years, by 50 basis points.

- The euro area, already in the midst of a policy easing cycle, is seeing growth after stagnation in 2023.

- In the UK, an uptick in services inflation meant the Bank of England did not cut rates at its September meeting.

The US Federal Reserve (Fed) has cut its federal funds rate for the first time in four years. The move signals the Fed’s confidence that US inflation is slowing, as well as a shift in focus to shore up the weakening US labour market. In kicking off its easing cycle, the US now joins the euro area and UK, where central banks had already begun cutting policy rates.

While the US, euro area and UK are seeing varying degrees of economic health, China may struggle to meet its growth target given lacklustre domestic demand. A strong, timely policy response will be required.

United States

The Fed cut its policy interest rate by 50 basis points (bps)1 but did so in the context of economic resilience rather than concerns about a material slowdown.

The Fed’s decision, announced on 18 September, marked a strong start to its easing cycle. The 50-bps reduction in the federal funds rate indicates a target range of 4.75%-5%. The Fed had resisted cuts at previous meetings, which allowed monetary policymakers to see more evidence of slowing inflation and gave them the confidence to cut by 50 bps rather than 25 bps.

At the midpoint of the year, GDP growth was tracking largely in line with Vanguard’s 2% outlook for 2024. The US economy grew more in the second quarter than previously thought, with real GDP rising by an annualised 3%. Strong consumer spending contributed to the growth.

The pace of headline inflation, as measured by the consumer price index (CPI), slowed again in the year to August to 2.5% compared with 2.9% in the year to July. Core CPI, which excludes volatile food and energy prices, rose by 3.2% in the year to August, little changed from July.

Recent data suggest softening in the labour market. There was a second consecutive month of below-consensus job growth, coupled with a recent pattern of downward revisions to already-announced totals. We expect job growth continuing to slow amid moderating economic activity, with the unemployment rate ending the year marginally above current levels (4.2% in August).

Euro area

The euro area is growing after stagnation in 2023. We expect steady—but not spectacular—growth in 2024 as restrictive monetary and fiscal policy constrain activity.

The European Central Bank (ECB) announced a 25-bps cut to its policy rate on 12 September. The decrease in the deposit facility rate, to 3.5%, was the second cut of a cycle that began in June with a similar 25-bps cut. Vanguard does not expect a further cut at the ECB’s October meeting, although we anticipate the easing cycle will resume with a 25-bps cut in December, followed by a quarterly cadence of 25-bps reductions in 2025.

The euro area economy grew again in the second quarter, with real GDP rising by 0.2% compared with the first quarter. This was despite an unexpected drag from Germany, where a rebound in the manufacturing sector remains elusive.

The pace of headline inflation slowed in August, driven by a drop in energy prices. Headline inflation slowed to 2.2% in the year to August—the slowest in three years—compared with 2.6% in the year to July. Core inflation, which excludes volatile food, energy, alcohol and tobacco prices, slowed marginally in August; however, services inflation remained sticky.

The unemployment rate returned to a record low of 6.4% on a seasonally adjusted basis in July, falling from 6.5% in June. We foresee little change to the unemployment rate into year-end.

United Kingdom

In the UK, the Bank of England (BoE) held rates steady at 5% in September after initially cutting in August. We expect rate cuts to resume in the fourth quarter and believe rates will end the year at 4.75%.

The BoE’s decision to keep rates unchanged reflects that risks to resurgent inflation remain, although services inflation, pay growth and GDP data have all undershot expectations since the bank’s last meeting.

GDP growth increased by 0.6% in the second quarter compared with the first. We expect the UK economy to moderate in the second half the year, growing by 1.2% for all of 2024.

The pace of headline inflation held steady at 2.2% in the year to August. Meanwhile, core CPI, which excludes volatile food, energy, alcohol and tobacco prices, jumped to 3.6% in the year to August, compared with 3.3% in the year to July. Vanguard expects core inflation to end 2024 around 2.8% and to hit the BoE’s 2% target by the second half of 2025.

Wage growth cooled to its slowest pace in more than two years in the May-July period, even as the unemployment rate fell to 4.1% and job vacancies decreased for a 26th consecutive reading during that period. We foresee the unemployment rate ending 2024 in the 4%-4.5% range.

China

Sluggish domestic demand has put China’s 2024 growth target of 5% at risk. Fiscal policy in the form of increased government loan issuance in August provides hope, but more of the same will likely be required in the months ahead.

Government loan issuance totalled 900 billion yuan in August, a significant ramp up compared with the 260 billion yuan issued in July. In order for the government to hit its 5% growth target for 2024, this is the type of timely policy response that will be required. On the monetary policy side, we expect the start of the Fed’s rate-cutting cycle could give the People’s Bank of China (PBoC) room to cut as well.

GDP grew by only 0.7% in the second quarter compared with the first and by 4.7% compared with the second quarter last year. Weaker-than-expected retail sales and industrial production figures suggest that China’s growth momentum slowed in August.

The pace of inflation, as measured by consumer prices, rose 0.6% in the year to August, below expectations and well below the 3% inflation target set by the PBoC. We expect inflation in 2024 to be mild, with headline inflation of 0.8% and core inflation, which excludes volatile food and energy prices, of just 1.0%.

The unemployment rate rose to 5.3% in August from 5.2% in July. Vanguard expects that rate to remain around current levels for the rest of the year.

The points above represent the house view of the Vanguard Investment Strategy Group’s (ISG’s) global economics and markets team as at 19 September 2024.

Asset-class return outlook

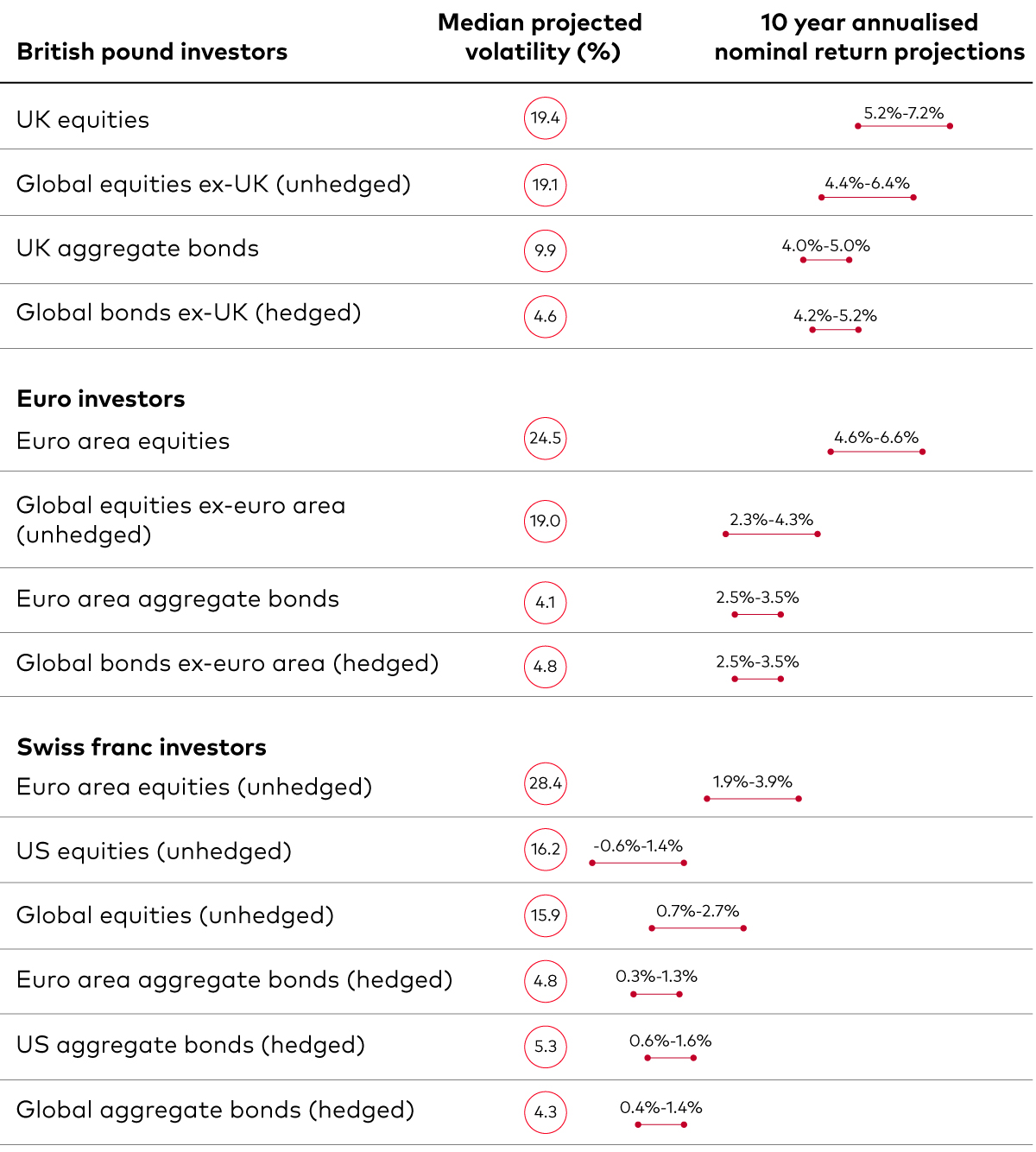

Vanguard has updated its 10-year annualised outlooks for broad asset class returns through the most recent running of the Vanguard Capital Markets Model® (VCMM), based on data as at 30 June 2024.

Our 10-year annualised nominal return projections, expressed for local investors in local currencies, are as follows2.

1 A basis point is one-hundreth of a percentage point.

2 The figures are based on a 2-point range around the 50th percentile of the distribution of return outcomes for equities and a 1-point range around the 50th percentile for fixed income. Numbers in parentheses reflect median volatility.

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time. The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include US and international equity markets, several maturities of the US Treasury and corporate fixed income markets, international fixed income markets, US money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

The primary value of the VCMM is in its application to analysing potential client portfolios. VCMM asset-class forecasts—comprising distributions of expected returns, volatilities, and correlations—are key to the evaluation of potential downside risks, various risk–return trade-offs, and the diversification benefits of various asset classes. Although central tendencies are generated in any return distribution, Vanguard stresses that focusing on the full range of potential outcomes for the assets considered, such as the data presented in this paper, is the most effective way to use VCMM output.

The VCMM seeks to represent the uncertainty in the forecast by generating a wide range of potential outcomes. It is important to recognise that the VCMM does not impose “normality” on the return distributions, but rather is influenced by the so-called fat tails and skewness in the empirical distribution of modeled asset-class returns. Within the range of outcomes, individual experiences can be quite different, underscoring the varied nature of potential future paths. Indeed, this is a key reason why we approach asset-return outlooks in a distributional framework.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

The information contained in this document is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

Issued in EEA by Vanguard Group Europe Gmbh, which is regulated in Germany by BaFin.

© 2024 Vanguard Group (Ireland) Limited. All rights reserved.

© 2024 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2024 Vanguard Asset Management, Limited. All rights reserved.

© 2024 Vanguard Group Europe Gmbh. All rights reserved.